.webp)

Global M&A performance in Q1 2026 showed fewer deals but larger checks. Total transactions dropped from 11,284 in Q4 2025 to 7,924, while aggregate deal value rose from $785.2B to $861.1B. This divergence shows where the money is going: fewer bets, bigger conviction, focused on strategic scale. If you’re a retail investor or allocator mapping M&A trends to your portfolio, that split matters more than any headline count because megadeals drive index-level returns while the shrinking small-deal tail signals risk aversion in the middle market.

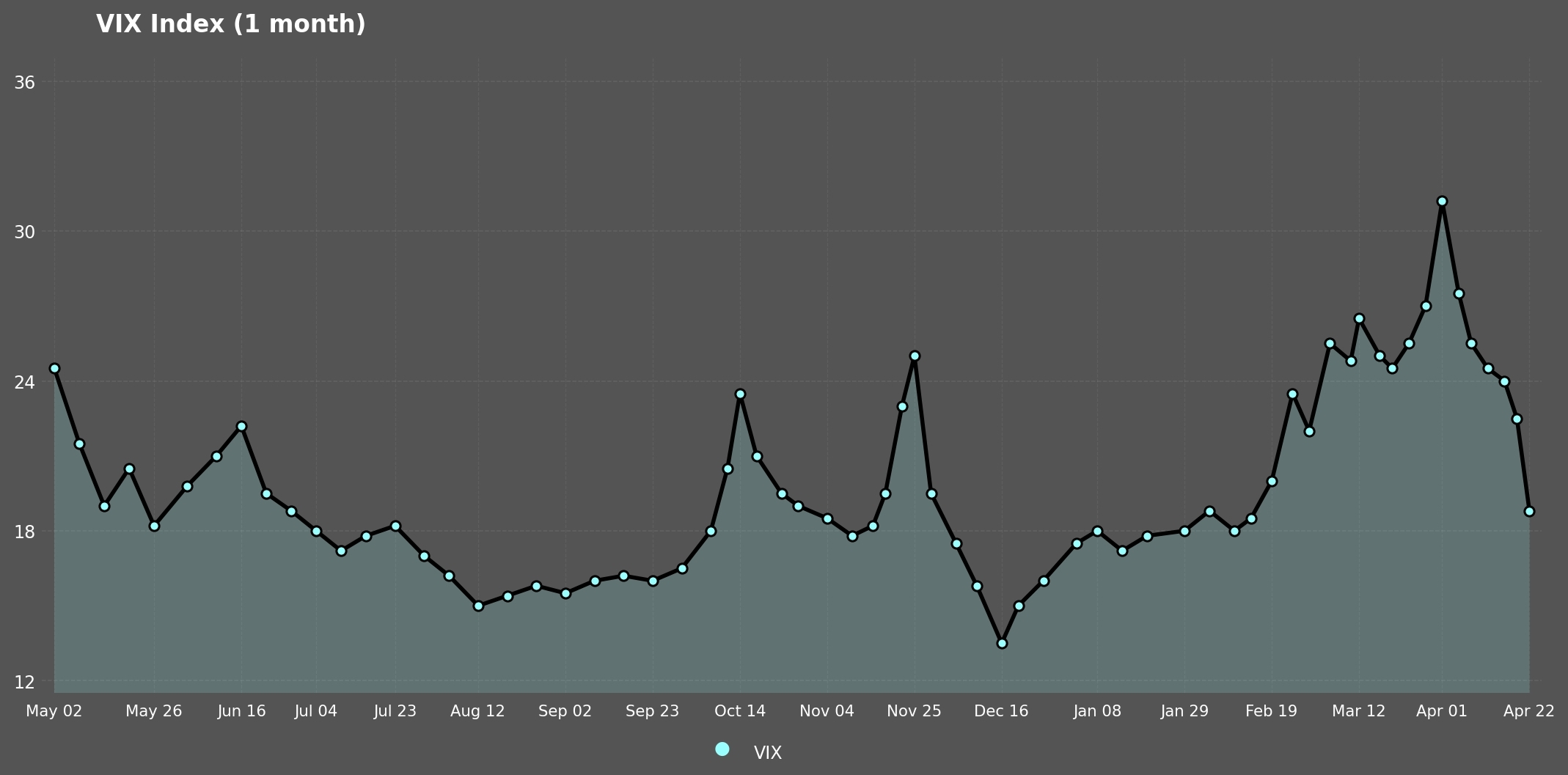

The quarter was ugly on almost every macro dial. The S&P 500 closed down 4.6%, the VIX spiked past 30, the Fed paused cuts, and consumer sentiment cratered due to the Iran conflict. Yet dealmakers wrote checks. Below, you’ll get the full macro picture, global M&A performance numbers, standout blockchain deals, and a forward look at what the next quarter likely holds for your capital.

The short answer: capital is available, volatility is elevated, and buyers are being selective. That combination tends to produce fewer but larger, more strategic deals, which is exactly what Q1 delivered.

The CBOE Volatility Index (VIX) climbed more than 40% versus Q4 2025, repeatedly breaching the 30 mark in March before retreating to 23.87 on April 3 after a Middle East de-escalation agreement. Readings above 25 generally signal high investor anxiety, and Q1 sat there for most of March.

The drivers were obvious: the US-Israel joint campaign against Iran that started February 28, tariff uncertainty, and a Fed that kept shifting the goalposts on rate cuts. Expect more turbulence in the next few months as Fed chair succession, energy prices, and trade policy all remain unsettled.

The benchmark closed the quarter at 6,528.52, down 4.6% from Q4 2025, per data tracked by S&P Dow Jones Indices. The index peaked at 6,845.50 in Q4 2025, making Q1 the worst start to a year since 2022. Energy led the winners. Tech and software got hammered.

For M&A performance, a declining index is a mixed signal: it depresses acquirer equity currency but compresses target valuations, bringing strategic buyers with clean balance sheets back to the table.

Nasdaq Inc. reported first quarter 2026 net revenue of $1.4B, flat versus Q4 2025 and up 14% year over year, with solutions revenue at $1.08B and annualized recurring revenue of $3.2B. The exchange operator benefited from higher trading volumes driven by the volatility spike.

Market infrastructure companies print money when others are panicking. That’s a useful hedge to remember when building an M&A-sensitive portfolio.

The Fed held the benchmark target range at 3.50% to 3.75% in March after three cuts in late 2025 dropped it from roughly 4.3%, according to St. Louis Fed FRED data. The effective rate tracked near 3.6% through Q1.

Here’s what matters for dealmakers: further cuts are postponed by at least six months as the central bank weighs inflation from the Iran war and elevated energy prices. FOMC participants now see just one more cut in 2026 versus the two markets had priced in. Higher-for-longer rates mean leveraged buyout math stays brutal, which is why strategic acquirers, not PE sponsors, drove most Q1 headline deals.

The US unemployment rate fell from 4.42% by end of Q4 2025 down to 4.32% in Q1 2026 per BLS data.

Don’t let the headline fool you. The drop came mostly from a 396,000 decline in the labor force. The prime-age hiring rate hit lows last seen during the COVID and GFC recessions. Tech and financial services shed jobs. You’re still watching AI chew through white-collar roles in real time.

That labor picture feeds directly into deal rationale: acquirers target AI-native platforms to do more with fewer people.

The University of Michigan Surveys of Consumers showed sentiment falling to 53.3 in March, down roughly 6% month over month and near record lows. The preliminary April reading plunged further to 47.6. Year-ahead inflation expectations rose throughout the quarter, reaching roughly 6.5% in early 2026 when accounting for the April spike, with more than 50% of consumers citing high prices tied to geopolitical tensions and tariffs.

Economic confidence is the oxygen of an active deal market. When consumers pull back, revenue forecasts compress, due diligence takes 60 days longer, and valuations get chopped. Weak sentiment is a headwind on M&A performance heading into Q2.

Dealmakers made fewer transactions but paid up for the ones they closed. That’s the story in a sentence. Now let’s get into the numbers.

Per S&P Global Market Intelligence, announced M&A volume fell from 11,284 transactions in Q4 2025 to 7,924 in Q1 2026. But aggregate value climbed to $861.1B, up from $785.2B. Against the longer tape, Q1 2026 stacks up surprisingly well:

That puts Q1 2026 higher than every comparable Q1 since 2021 and higher than the prior quarter.

Don’t just count deals. Watch where the dollars concentrate. There’s a K-shaped market where megadeals do the heavy lifting while the small to mid-market stalls.

Cross-border M&A dropped from 2,900 deals in Q4 2025 to 2,002 in Q1 2026. Aggregate cross-border value, however, only fell 7.5%. Small to mid-market international acquisitions got deprioritized as tariff policy, sanctions exposure, and the Iran conflict made foreign diligence harder. But at the top of the market, buyers kept writing checks for strategic cross-border scale.

Blockchain M&A delivered some of the most interesting stories of the quarter. Prediction markets, bank-fintech convergence, decentralized social, regulated payments, and ecosystem rescue operations all saw meaningful consolidation. Here’s what actually happened and why each deal matters to your strategy.

On March 18, prediction market giant Polymarket announced the all-stock acquisition of DeFi infrastructure startup Brahma. Terms weren’t disclosed, but the deal lands against Polymarket’s reported ~$20B valuation. Brahma, founded in 2021, had processed more than $1B in DeFi transaction volume and will wind down its standalone Console and vault products within 30 days to focus entirely on Polymarket’s execution stack.

Polymarket is racing Kalshi for dominance in regulated prediction markets, and if your betting app feels like a trading app instead of a blockchain protocol, you win. The takeaway is simple: infrastructure acquisitions are now defensive moats in crypto, not nice-to-haves.

On January 22, Capital One Financial Corporation (NYSE: COF) announced it would buy fintech Brex in a 50/50 cash-and-stock transaction valued at $5.15B. The deal is expected to close mid-2026 and is being billed by Brex as the largest bank-fintech deal in history. Brex’s last private valuation was $12.3B in a 2022 Series D-2, so this is less than half its peak mark.

This is the playbook for bank-fintech convergence in 2026: buy distressed unicorns at half-price, plug in the balance sheet, and compete with Ramp and JPMorgan Payments at scale.

On January 21, Haun Ventures-backed Neynar acquired the Farcaster social protocol from Merkle Manufactory at a reported ~$1B valuation. Neynar takes over the protocol contracts, code repositories, the Farcaster app, and Clanker, the AI token launchpad that has generated over $50M in protocol fees since Farcaster acquired it in October 2025.

Strategically, this is a consolidation of power in decentralized social. Neynar already ran the APIs. Now it owns the network. This is a clear signal: venture-funded social networks with weak revenue will keep getting absorbed by their infrastructure providers. Watch for the same pattern across gaming and DePIN.

On March 11, Ripple announced plans to acquire BC Payments Australia Pty Ltd, a subsidiary of European payments giant Banking Circle, to secure an Australian Financial Services License (AFSL). The deal is expected to close in April 2026. Ripple’s APAC payments volume nearly doubled year over year in 2025, and the company processed roughly $100B across 60 markets in the trailing period.

Australia is tightening its regulatory regime. Starting June 30, 2026, crypto firms operating there must hold an AFSL. Rather than apply from scratch, Ripple bought a firm that already holds one. Honestly, this is a masterclass in regulatory arbitrage. Ripple now holds more than 75 licenses globally and raised $500M at a $40B valuation in November 2025, making it one of the world’s most regulated and well-capitalized crypto companies.

The so-what is blunt: in 2026, licenses are moats. If you can’t build one, buy one.

On March 10, the Jito Foundation acquired SolanaFloor after the site went dark following a $27M exploit at its parent Step Finance. The Step Finance treasury hack on January 31 drained roughly 261,854 SOL, worth about $40M, forcing the shutdown of SolanaFloor and Remora Markets. Terms weren’t disclosed. SolanaFloor’s editorial team was absorbed and will operate independently under Jito’s ownership.

When a major chain loses its leading independent media voice, institutional allocators get jumpy. Jito stepped in to preserve information infrastructure, which is a weirdly mature move for crypto. Foundations buying public goods to protect the network thesis is, frankly, a trend worth watching. If you operate in a crypto ecosystem, expect more foundation-led rescue M&A.

We work live deals across crypto media, agentic infrastructure, OTC desks, and regulated exchanges, so what you're about to read isn't a forecast built from headlines. It's what we're actually seeing in active processes right now.

We expect fewer deals overall, but Q2 will be more active than Q1 in the $5M to $30M range. The freeze in the small- to mid-market was a sentiment reaction, not a structural one. As geopolitical noise stabilizes and buyers get clarity on Fed timing, compressed valuations will pull strategic buyers off the sideline. Acquire.Fi is currently running active sell-side processes across crypto media, agentic infrastructure, OTC desks, and regulated exchanges, and buyer engagement across all four verticals has increased month over month since January.

In the second half of 2025, sellers were still anchoring to 2021 multiples. That's largely broken. Most founders we work with have adjusted expectations to reflect current market reality. The remaining gap is concentrated in cash versus equity structure disputes, not headline valuation. Buyers want more cash certainty. Sellers want upside protection. Deals that bridge that through earnouts or milestone-based structures are moving. Deals that don't are stalling.

AI has cut our research and buyer targeting time significantly. Buyer profiling, deal teaser drafts, and comp analysis that used to take days now take hours. On the buyer side, we’re also seeing more sophisticated AI-driven screening, which means your deck and financial model must hold up to automated scrutiny before you get a human call. Firms that show up with clean data rooms and clear AI-augmentation narratives are getting faster LOIs.

Deals and valuations were affected by trends in AI. We paused engagement on one target where AI tools flagged material discrepancies between publicly stated metrics and actual platform data during early diligence. On the upside, we've seen AI-native deals command a meaningful premium, specifically platforms where the technology layer is defensible and not easily replicated. Our current mandate in agentic DeFi yield infrastructure is a direct example: the combination of $4B in transaction volume, 3,500 active agents, and $50M in institutional MOUs is the kind of profile that drives acqui-hire interest from L1s and major exchanges precisely because it's difficult to rebuild from scratch.

The three we see most often across our pipeline:

The Q1 data points in a clear direction, and the deals we're currently running confirm it. Here's where we think the market moves next and what you should be positioning for before it happens.

Every regulated deal we're working on is attracting more buyer interest than unlicensed equivalents with comparable revenue. VARA in Dubai, MiCA exposure in Europe, FINMA in Switzerland, and AFSL in Australia are all drawing strategic buyers who cannot or do not want to wait two years to build licensing themselves. Ripple's acquisition of BC Payments Australia is the clearest public example, but this is happening at every deal size below the headlines. Expect license stacks to become the single largest driver of valuation premium in Q2.

Clean exits are harder to justify for buyers when the product is early. Retaining the team through structured employment contracts tied to integration milestones will become standard deal architecture for sub-$15M technical acquisitions. We are already structuring deals this way.

Distribution is scarce and expensive to rebuild. Platforms with 1M-plus engaged audiences, strong domain authority, and recurring ad or subscription revenue are attractively priced right now. Buyers are motivated. We expect to see several deals close in this vertical in Q2.

Dubai and Abu Dhabi are actively positioning as acquisition hubs for Web3 infrastructure. VARA licensing, favorable tax treatment, and capital availability from regional family offices and sovereign-adjacent funds are all pulling deal activity toward the region. Our team is seeing this directly across multiple mandates currently in process.

Buyers will regret overpaying for a community without revenue. Token-gated platforms, DAO treasuries, and social protocols with large user counts but no defensible monetization are being shopped aggressively. The Neynar-Farcaster deal will encourage a wave of similar pitches. Most will not hold up to diligence. Buyers who skip revenue quality checks in favor of engagement metrics will regret it before Q3.

With deep roots in traditional finance and the digital asset industry, Acquire.Fi operates as a specialist M&A advisory firm. Coverage spans M&A, secondaries, OTC, and capital markets advisory across digital assets and frontier tech. Decades of combined experience across every stage of the deal lifecycle.

.webp)