.webp)

ESOP stands for Employee Stock Ownership Plan. It is a qualified retirement plan that gives you an ownership stake in your company, funded by your employer rather than your paycheck. You don’t contribute any of your own money to get shares.

But don’t confuse ESOP with employee stock option plans. Stock options give you the right to buy shares at a fixed price in the future, so you pay out of pocket to exercise them. An ESOP allocates shares directly into your account over time at no cost. The distinction matters because the financial risk is different.

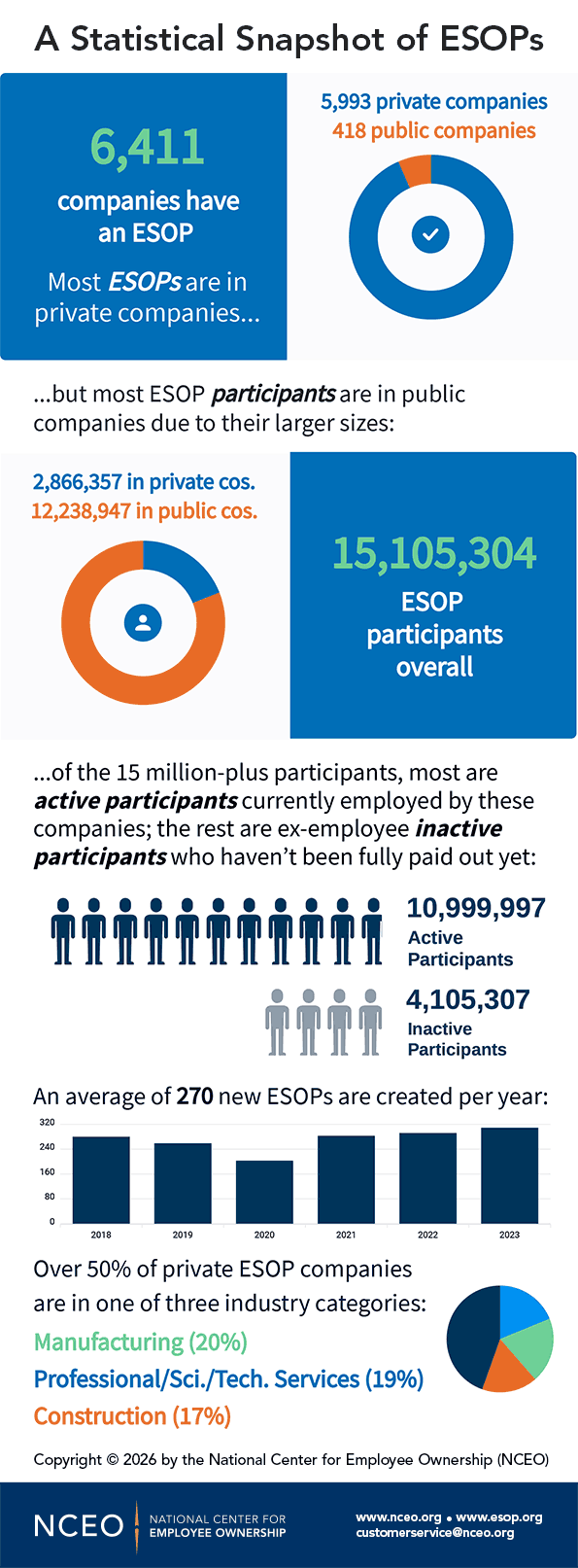

As of 2026, more than 15 million Americans participate in an ESOP, making it the largest form of employee ownership in the United States.

If your employer offers an ESOP or you’re considering a job at a company with one, having full grasp on how it works directly affects your retirement outcome. This isn’t just a perk. It’s real wealth accumulating in your name, and ESOP taxation, vesting rules, and distribution timing determine how much you keep.

The U.S. Securities and Exchange Commission classifies an ESOP as a retirement plan, the same legal category as a 401(k). That puts it under the Employee Retirement Income Security Act of 1974 (ERISA), which legally requires your company to act in your best financial interest when managing the plan. You have real protections here. Your employer cannot simply do whatever it wants with those shares.

An ESOP works by having your company set up a trust, fund it with cash or stock, and gradually allocate shares into individual employee accounts as you meet service and vesting requirements. Think of the trust as a holding tank: shares flow in from the company and slowly drain into your personal account based on how long you’ve worked there and what you earn.

Here’s the typical sequence for how does an ESOP work in practice:

According to the National Center for Employee Ownership, more than 90% of ESOPs are in private companies. That means most employees receive cash at distribution because there’s no public exchange to sell shares on directly.

You don’t own your ESOP shares outright from day one. Shares vest over a schedule your company defines, subject to ERISA minimum standards. If you leave before you’re fully vested, you forfeit the unvested portion. That’s a deliberate design, not an oversight. The longer you stay, the more you own. That’s exactly what makes an ESOP one of the more powerful wealth-building tools available to ordinary employees.

The primary purpose of an employee stock ownership plan, from a company’s perspective, is to give a departing business owner a tax-advantaged way to sell their company to the employees who built it. About two-thirds of ESOPs are set up for exactly this reason. But what that means for you as an employee is that you become a genuine owner of the business, with a financial stake in how well it performs.

ESOPs serve several overlapping purposes that directly affect you:

ESOPs are most common in closely held private companies across manufacturing, construction, professional services, and retail. But the structure is flexible enough to show up across a wide range of industries and company sizes, including some you almost certainly recognize.

Some of the most recognizable employee-owned companies in the United States run under an ESOP structure. Here are a few examples you’ve probably heard of:

Public companies use ESOPs too, though they represent only about 5% of all ESOP plans. In publicly traded companies, the ESOP often functions as a 401(k) match vehicle, where your employer contributes its own stock to your retirement account instead of cash.

Your industry and company size shape how much your ESOP is likely worth at retirement. Private company ESOP shares are valued annually by an independent appraiser, so your account balance grows or shrinks based on company performance, not stock market swings. That insulation from market volatility is a feature but also means your retirement is heavily tied to one company. Keep that concentration risk in mind.

ESOP taxation is genuinely favorable for employees. You pay no tax while your shares accumulate. You only owe taxes when you take distributions, and even then, you have options to defer further.

Your company’s contributions to your ESOP account are not taxed as income when they’re made. The shares sit in the trust, grow in value, and accumulate in your account entirely tax-deferred. That’s the same basic advantage as a traditional 401(k), except you didn’t have to contribute anything to get it.

When you leave the company or retire and receive your ESOP payout, it’s treated as ordinary income and taxed at your regular income tax rate. You can avoid that immediate tax hit by rolling your distribution into an IRA or another qualified retirement plan within 60 days, per IRS rules. That keeps the money growing tax-deferred until you need it.

If you take an early distribution before age 59½ without rolling it over, you’ll owe a 10% penalty on top of ordinary income taxes, with narrow exceptions for disability or death under IRS guidelines. Plan accordingly before you leave a job.

If your company’s owner sells to an ESOP under IRC Section 1042, they can defer capital gains taxes on the sale proceeds by reinvesting in other qualifying securities. This matters to you as an employee because it makes employee ownership transactions more attractive to sellers, increasing the number of companies that choose an ESOP over a sale to private equity. Your chances of ending up at an ESOP company go up.

If your employer is an S corporation with an ESOP, the ESOP’s share of company profits is not subject to federal income tax. A 100% ESOP-owned S corporation pays no federal corporate income tax on those earnings. Those tax savings can be reinvested in the business or used to pay down ESOP debt faster, which accelerates how quickly shares are released into your account.

The regulations around an employee stock ownership plan exist primarily to protect you, not to create paperwork for its own sake. Understanding what your company must do on your behalf helps you know whether your plan is being run correctly.

Every private company with an ESOP must have an independent appraiser determine the fair market value of its stock at least once per year. That appraised value is what your account balance is based on and what you get paid when you leave. The appraiser must be genuinely independent, not someone with a financial interest in inflating or deflating the number.

The regulatory standards around this valuation are actively in flux. On January 16, 2025, the U.S. Department of Labor released long-awaited proposed regulations defining exactly how valuations must be conducted. Those proposals were pulled four days later when the Trump administration froze all pending regulations. Because Congress mandated this guidance through the SECURE 2.0 Act of 2022, clearer rules are expected to reemerge. Until then, your plan’s appraiser works from the 1988 DOL proposed guidance and Revenue Ruling 59-60 as the unofficial standard.

Your employer has annual obligations that ensure your plan stays qualified and your benefits are protected. These include:

If your employer is not meeting these obligations, that’s a red flag. You can verify your plan’s filings using the Department of Labor’s public Form 5500 search tool.

When you leave the company, your employer must buy back your vested shares at fair market value. This repurchase obligation is a legal requirement, not optional. But companies that haven’t planned well can struggle to fund large distributions when many employees retire at once. If you’re at a maturing ESOP company, ask your plan administrator how the repurchase obligation is funded. Your retirement depends on it.

Some companies offer both an employee stock ownership plan and Incentive Stock Options (ISOs), particularly for senior employees or key hires. If your employer offers you both, understanding ESOP vs ISO helps you make smarter decisions about your total compensation.

The practical takeaway from ESOP vs ISO: an employee stock ownership plan builds retirement wealth passively with no cost or active decision-making required from you. An ISO requires you to manage exercise timing, holding periods, and the AMT risk to capture the tax benefit. Both can be valuable, but they serve different financial goals. Our separate guide about Incentive Stock Options breaks down the mechanics in more detail if you’re weighing both options.

→ Learn more about other types of equity compensation.

You generally can’t access your ESOP shares while employed. ESOP distributions are triggered by qualifying events: retirement, resignation, termination, disability, or death. Federal law and your plan document determine when you get paid and in what form.

When you leave the company, your vested ESOP account is distributed to you in one of three ways:

Once you reach age 55 with at least 10 years of ESOP participation, federal law gives you the right to redirect up to 50% of your ESOP account balance into other investment options within the plan. This is not a cash-out but a reallocation that reduces your exposure to a single employer’s stock. Since your ESOP may represent most of your retirement savings at that stage, taking advantage of this window is important.

If you receive a lump-sum ESOP distribution that includes company stock, you may qualify for Net Unrealized Appreciation (NUA) treatment. Instead of paying ordinary income tax on the full appraised value of the shares, you pay ordinary income tax only on the original cost basis. The appreciation is taxed at long-term capital gains rates when you sell. Rolling the distribution into an IRA defers all taxes but forfeits the NUA advantage, so you eventually pay ordinary income rates on the entire amount. Talk to a tax advisor before you decide. The difference in your effective tax rate can be substantial depending on how much the stock has appreciated.

→ Additional reading: ESOP vs ESPP

With deep roots in traditional finance and the digital asset industry, Acquire.Fi operates as a specialist M&A advisory firm. Coverage spans M&A, secondaries, OTC, and capital markets advisory across digital assets and frontier tech. Decades of combined experience across every stage of the deal lifecycle.

.webp)

{kind=link}